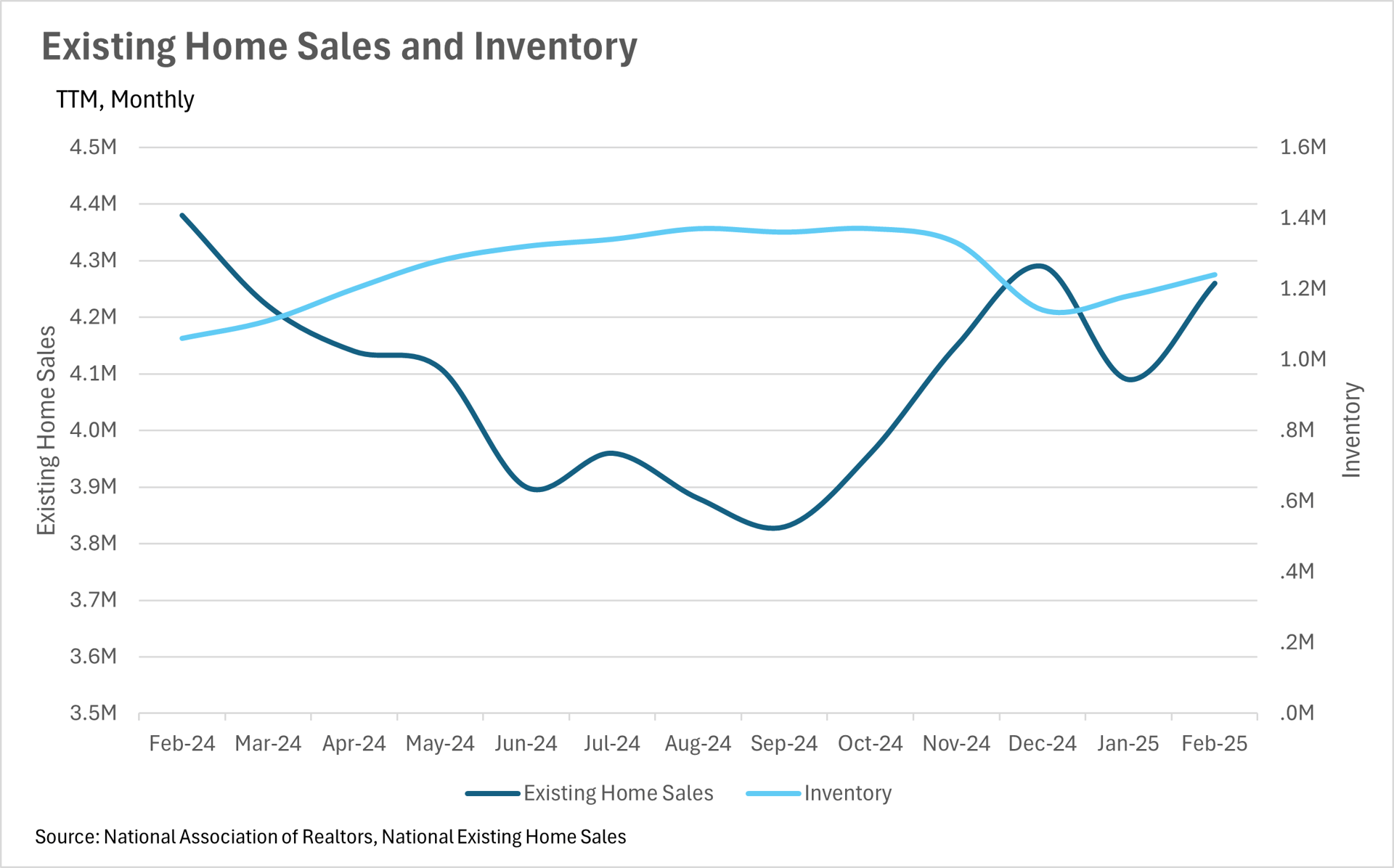

Although we are just about to exit the slow season for real estate sales, things are looking great overall. We saw a slight decrease in the number of sales on a year-over-year basis in February, with there being 4,260,000 sales in February 2025, compared to 4,380,000 in February 2024. However, on the flip side, we saw considerably more inventory added this year, with 1,240,000 homes on the market in February of this year, compared to 1,060,000 homes on the market around this time last year.

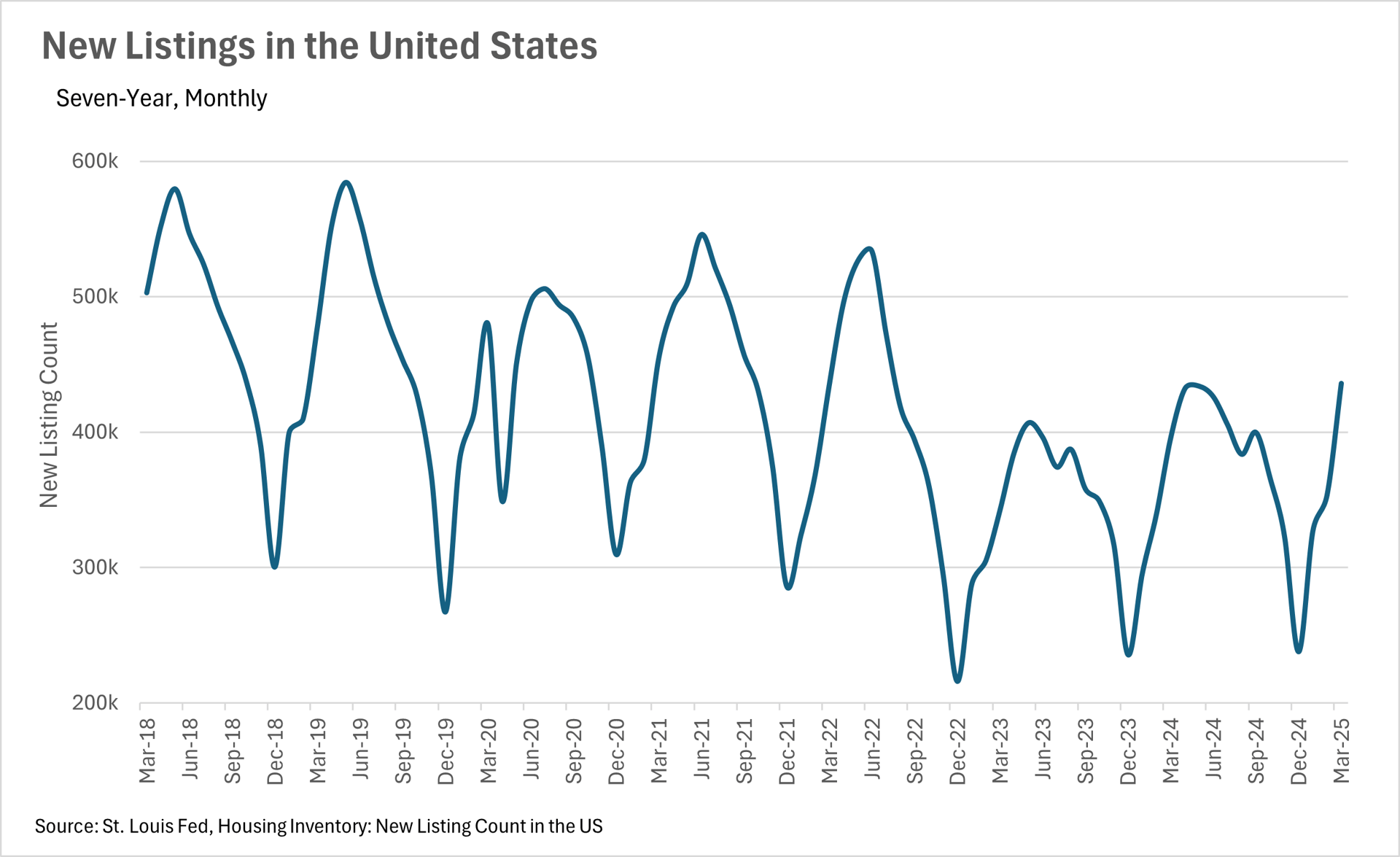

This means that all over the country, buyers have many more options than in recent years, which may lead to listings sitting on the market for a bit longer than what we’ve seen over the past couple of years. When you couple this with the fact that there are more new listings being added to the market, with just over 10% more listings added in March of 2025, compared to March of 2024, we might see some power start moving away from sellers to the buyers.

Additionally, this uptick in new listings might be an indication that sellers are starting to accept the fact that considerably lower mortgage rates aren’t coming anytime soon. Although many were holding out hope over the course of the past couple of years, the Fed has made it very clear that they’re not looking to drop rates by a considerable margin anytime soon. This, of course, means that prospective sellers have an important choice to make - whether they should sell, or continue holding out. From the data that we’re seeing, it seems that many sellers are beginning to choose the former option!

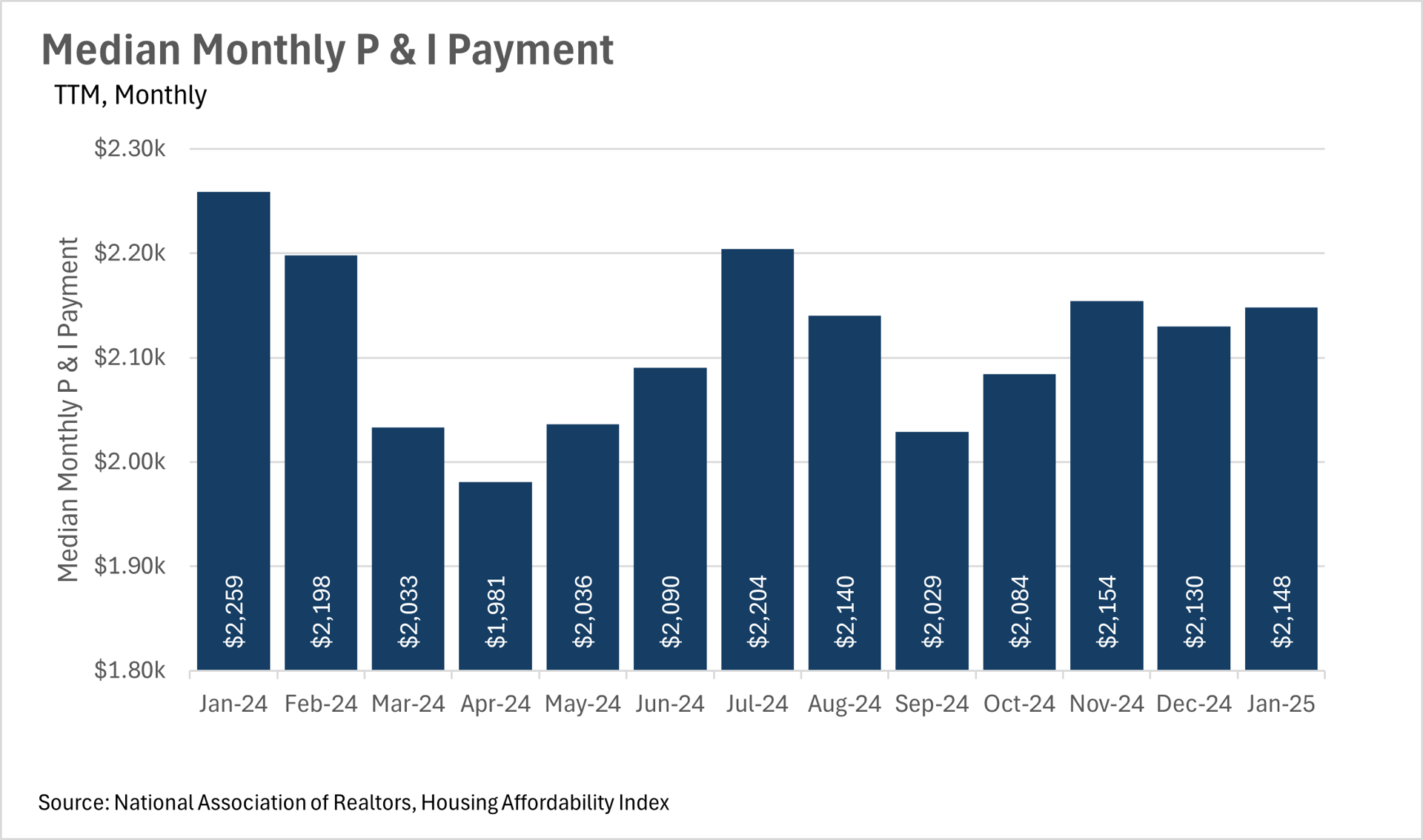

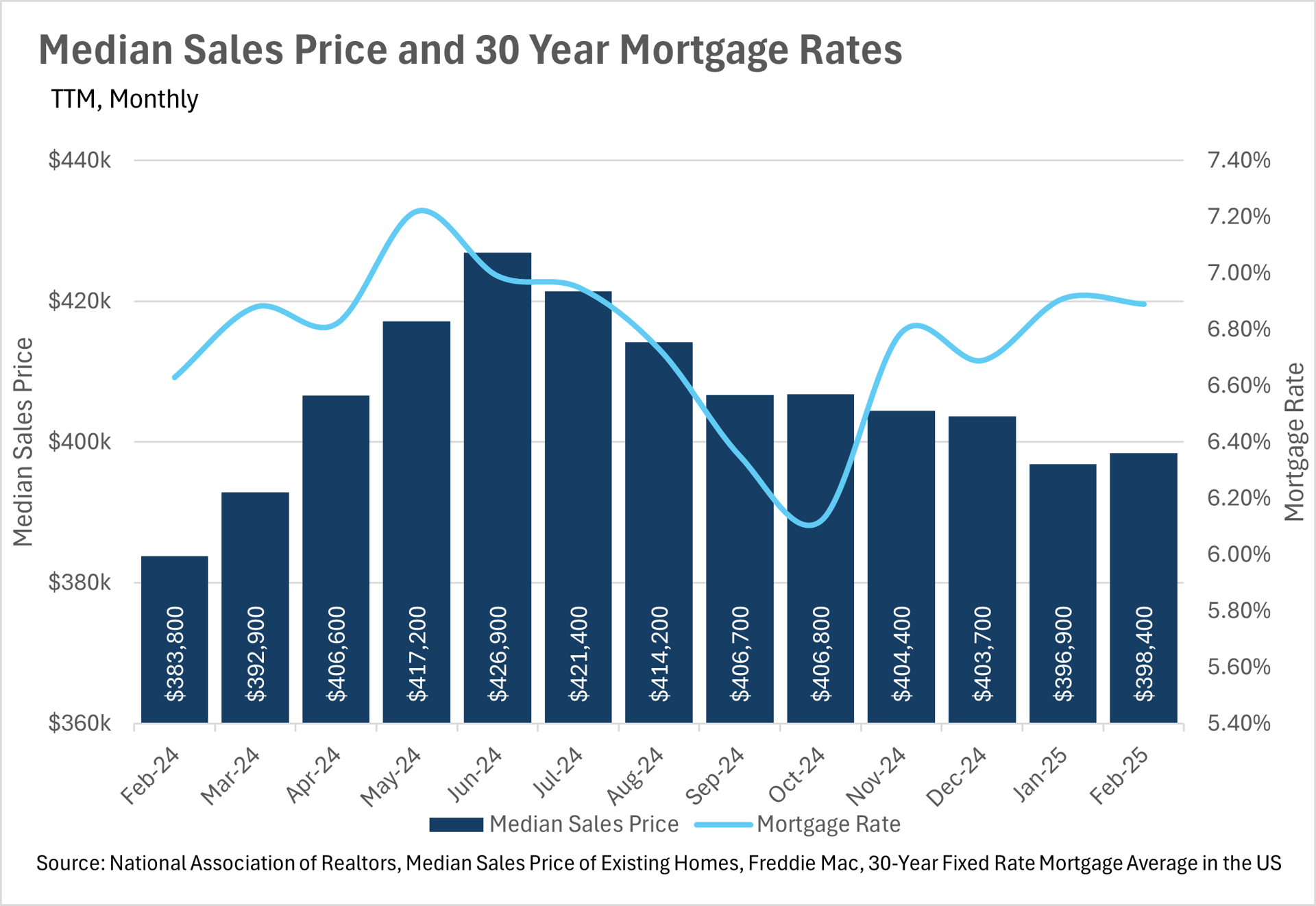

When turning to affordability, we saw a rather interesting phenomenon - median monthly P&I payments decreased by nearly 5%, all while interest rates and median sale prices increased by just under 4%. This likely means that there was a considerable cohort of homeowners out there that locked in rates toward the end of 2023 when rates were at a local high, and recently refinanced when rates came down a bit. The median consumer having an additional $100 in their pocket each and every month is a great thing for the economy, especially when we face economic uncertainty, tariffs, and ever-changing geopolitics!

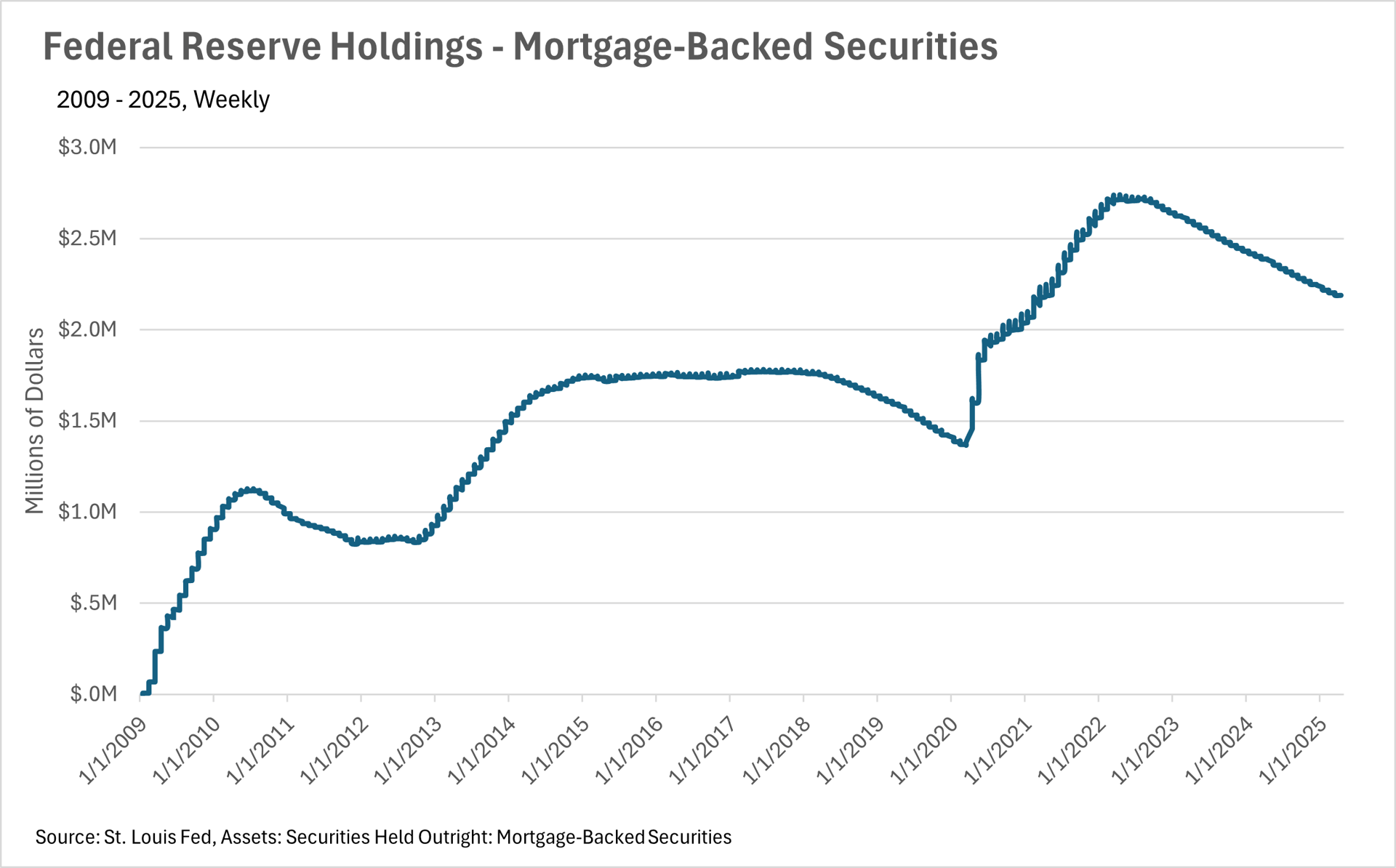

Lastly, it’s important to note that it’s business as usual in terms of the Federal Reserve. In their recent FOMC meeting, they decided to hold the federal funds rate firmly where it has been over the past couple of months. Fed officials also indicated that they are not in a rush to lower rates by a considerable margin anytime soon. However, that could always change, as we’re living in an incredibly dynamic era right now! Additionally, the Fed is continuing to offload mortgage-backed securities at a steady pace!

Ultimately though, this is just what we’re seeing at a national level. As we all know, real estate is an incredibly localized industry, so knowing what’s going on in your own market is pivotal. Below is our local lowdown, that outlines everything you need to know about what’s happening around you in your neighborhood and surrounding areas!

Big Story Data

The Local Lowdown

-

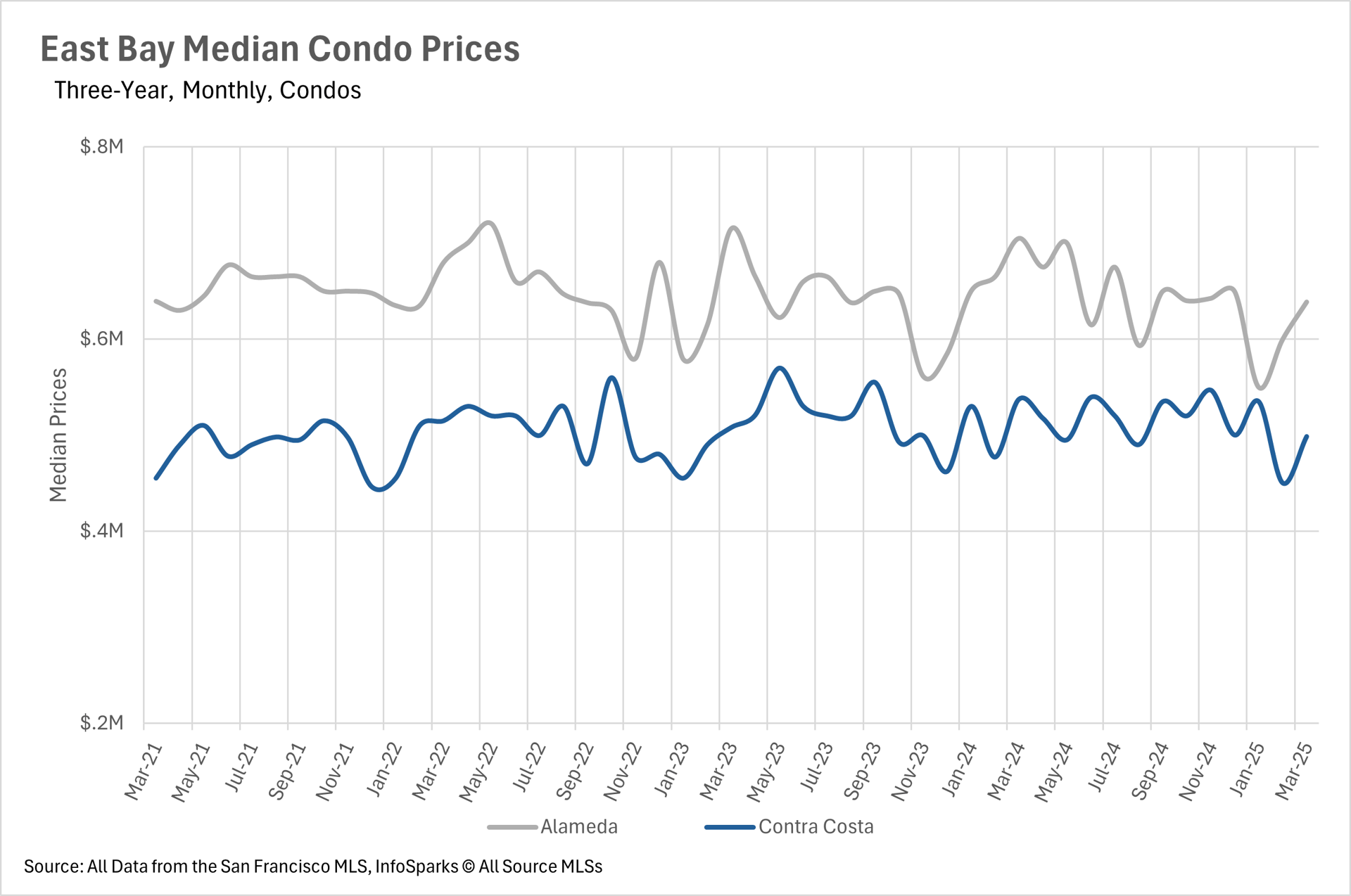

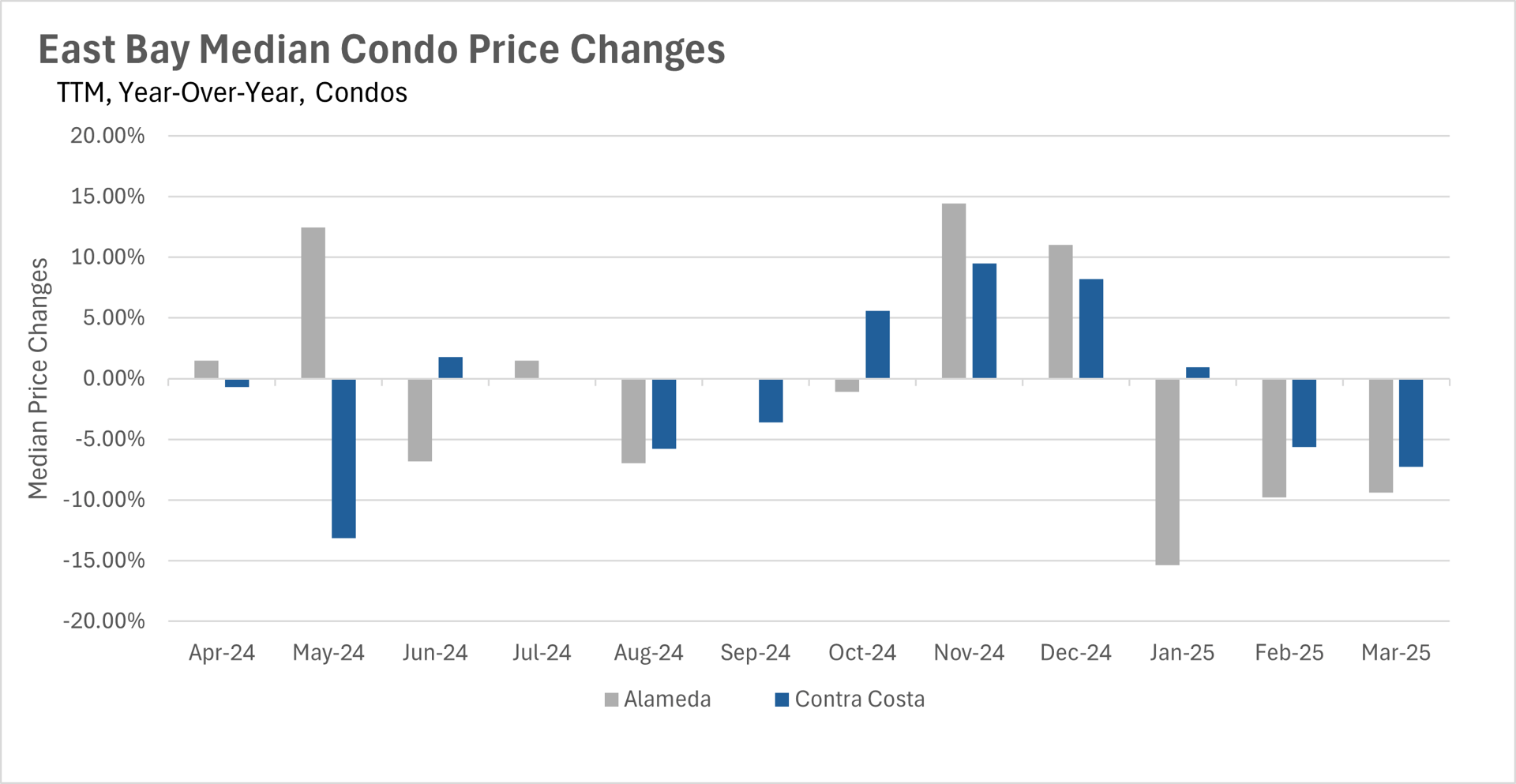

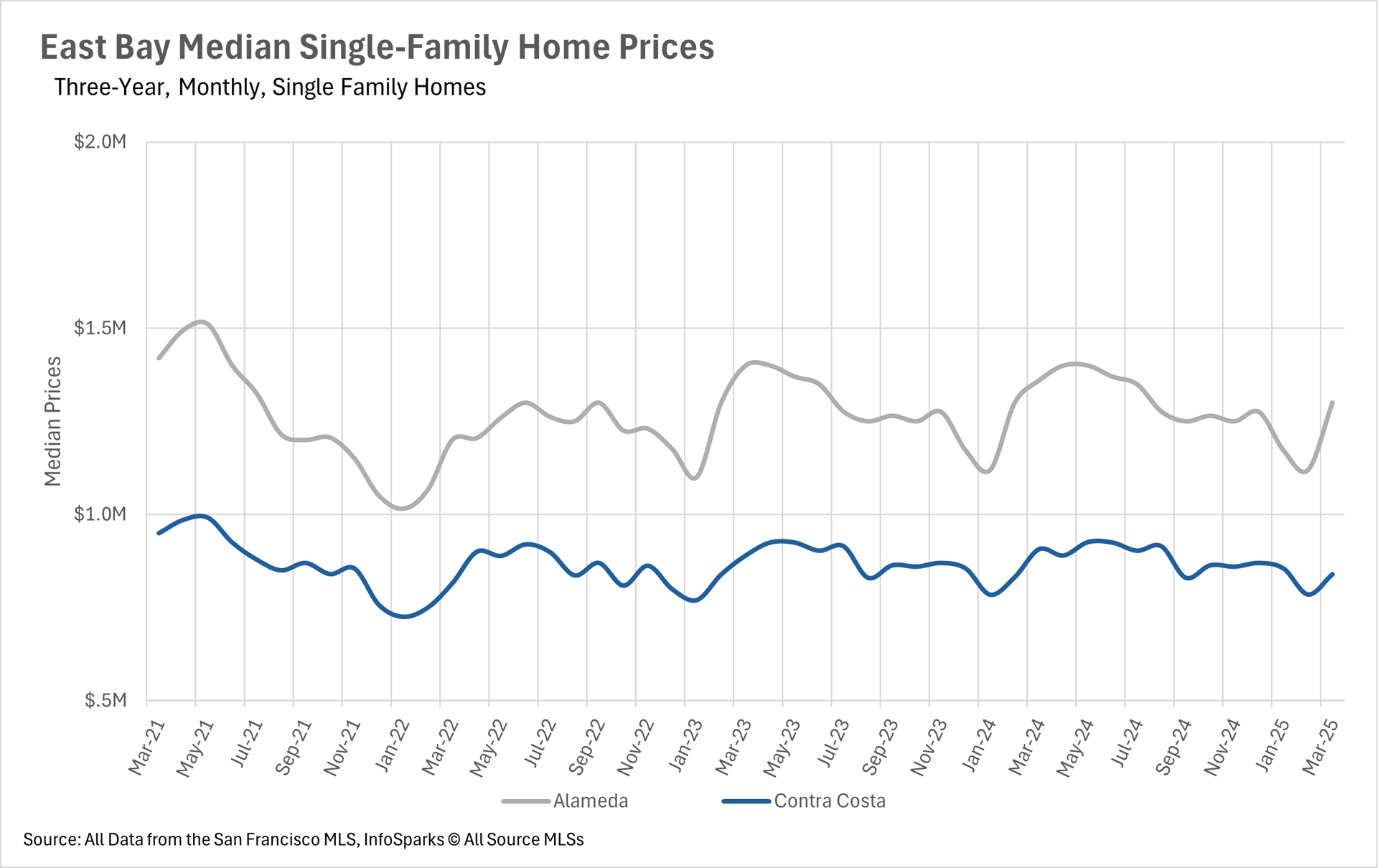

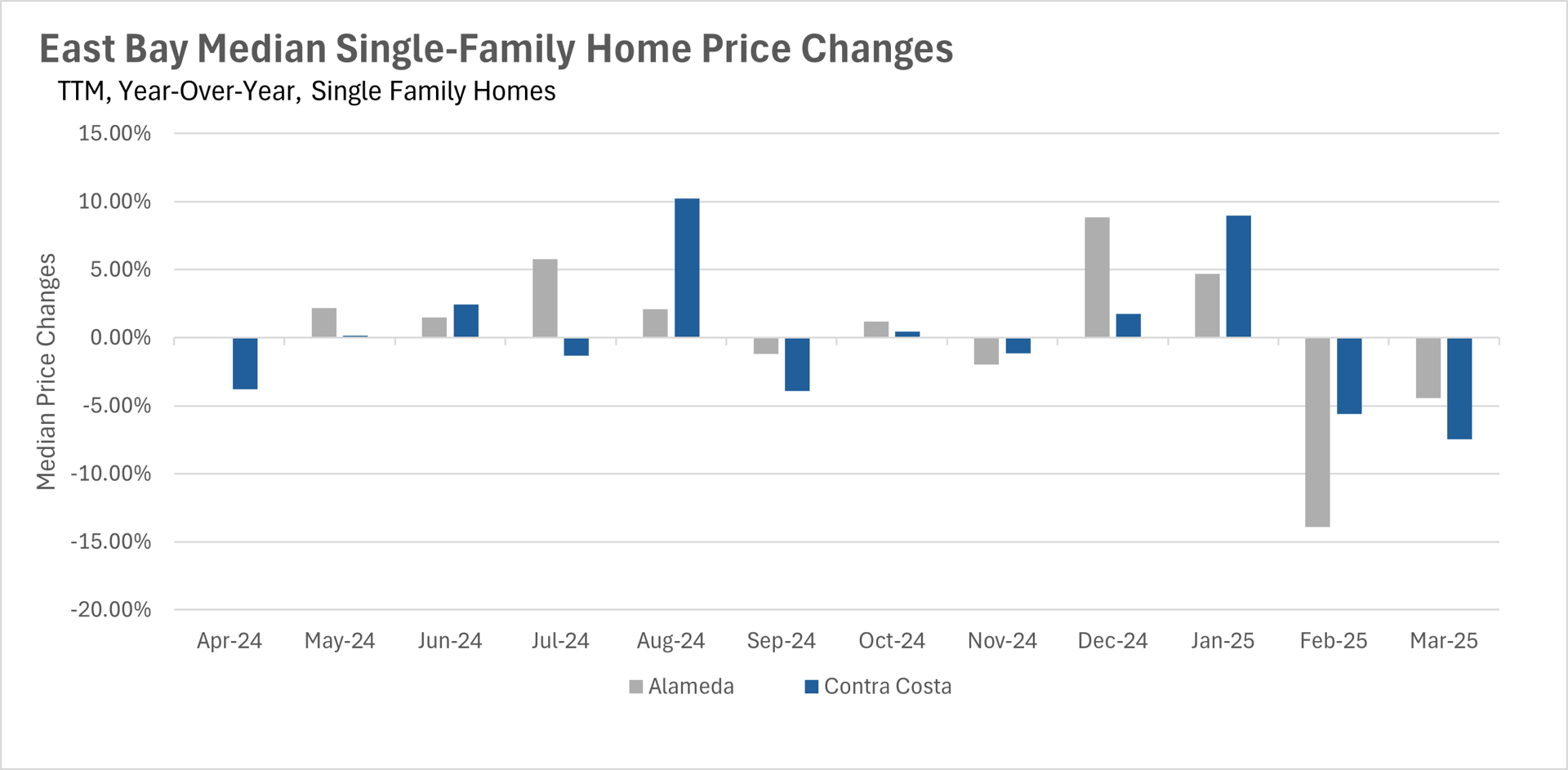

Median sale prices fell slightly on a year-over-year basis in the East Bay.

-

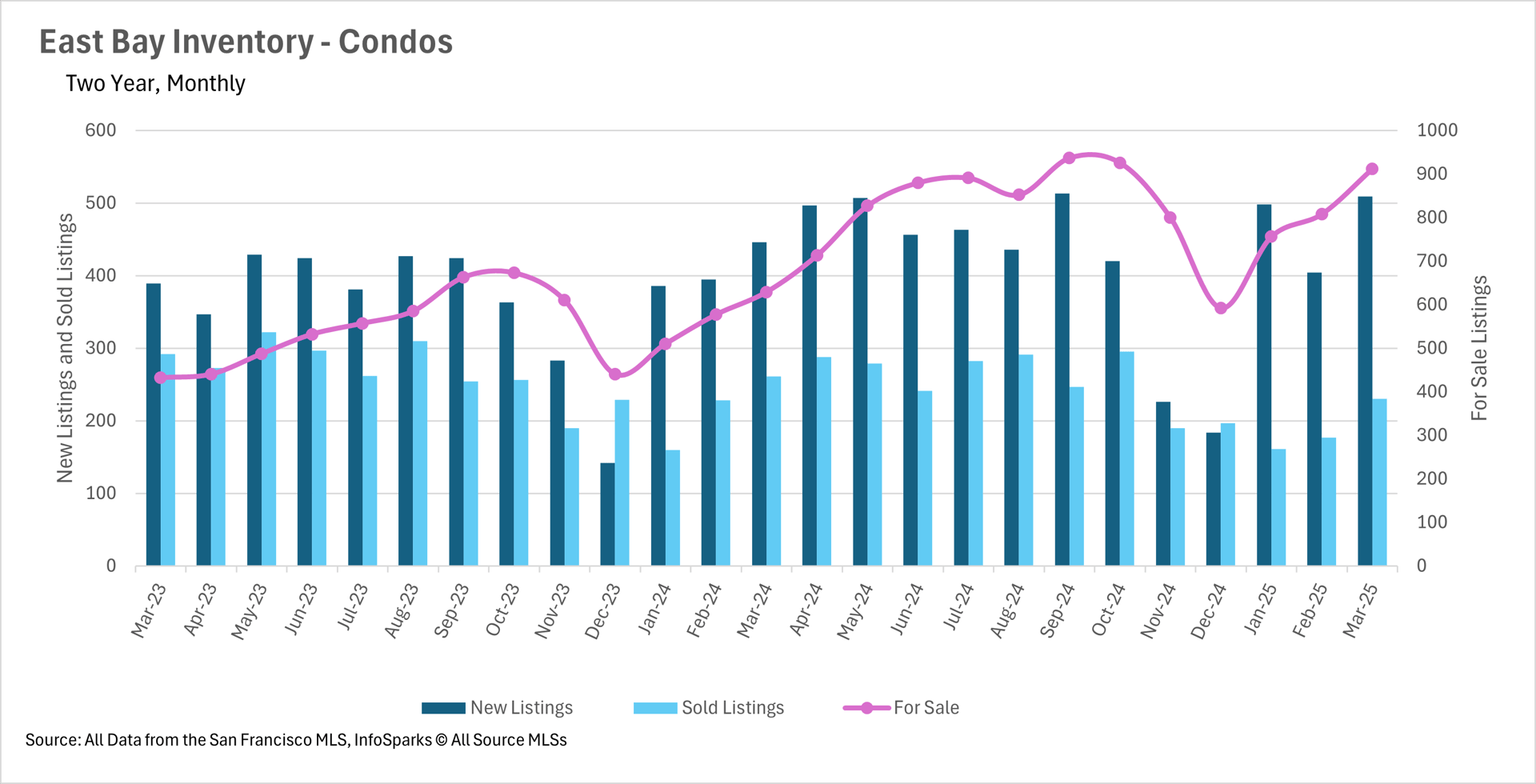

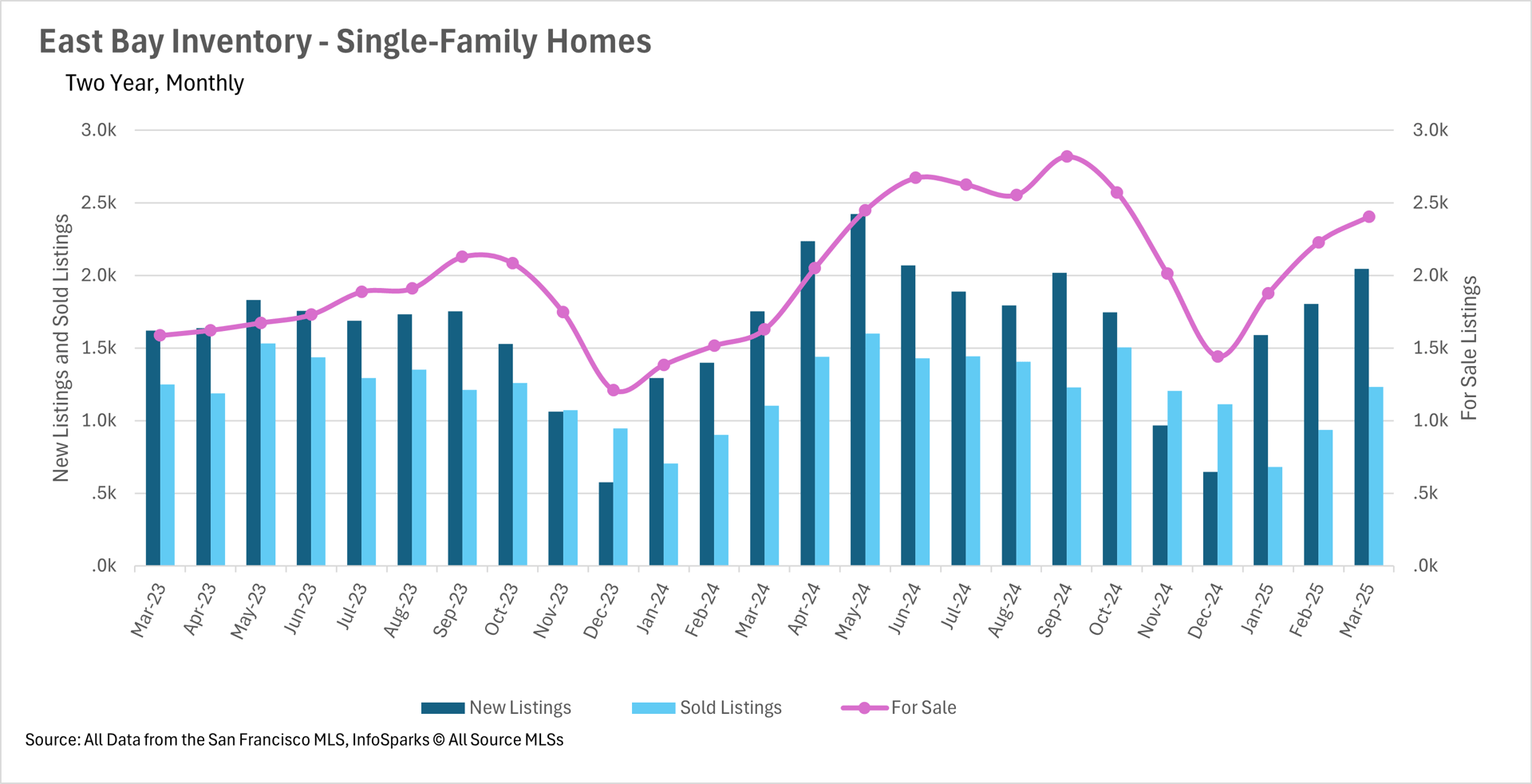

Inventories increased by a substantial margin, as new listings have flooded the market over the past couple of months.

-

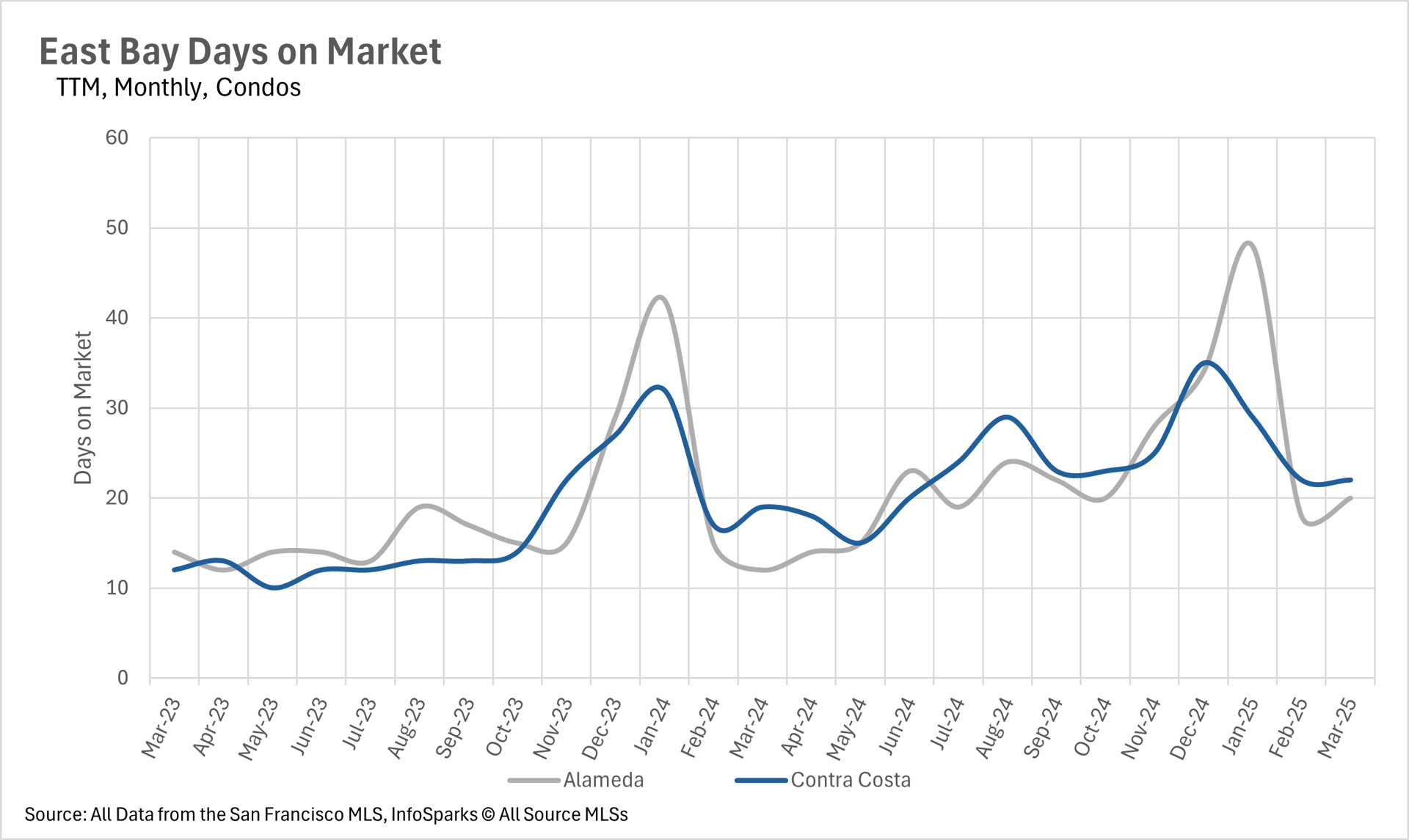

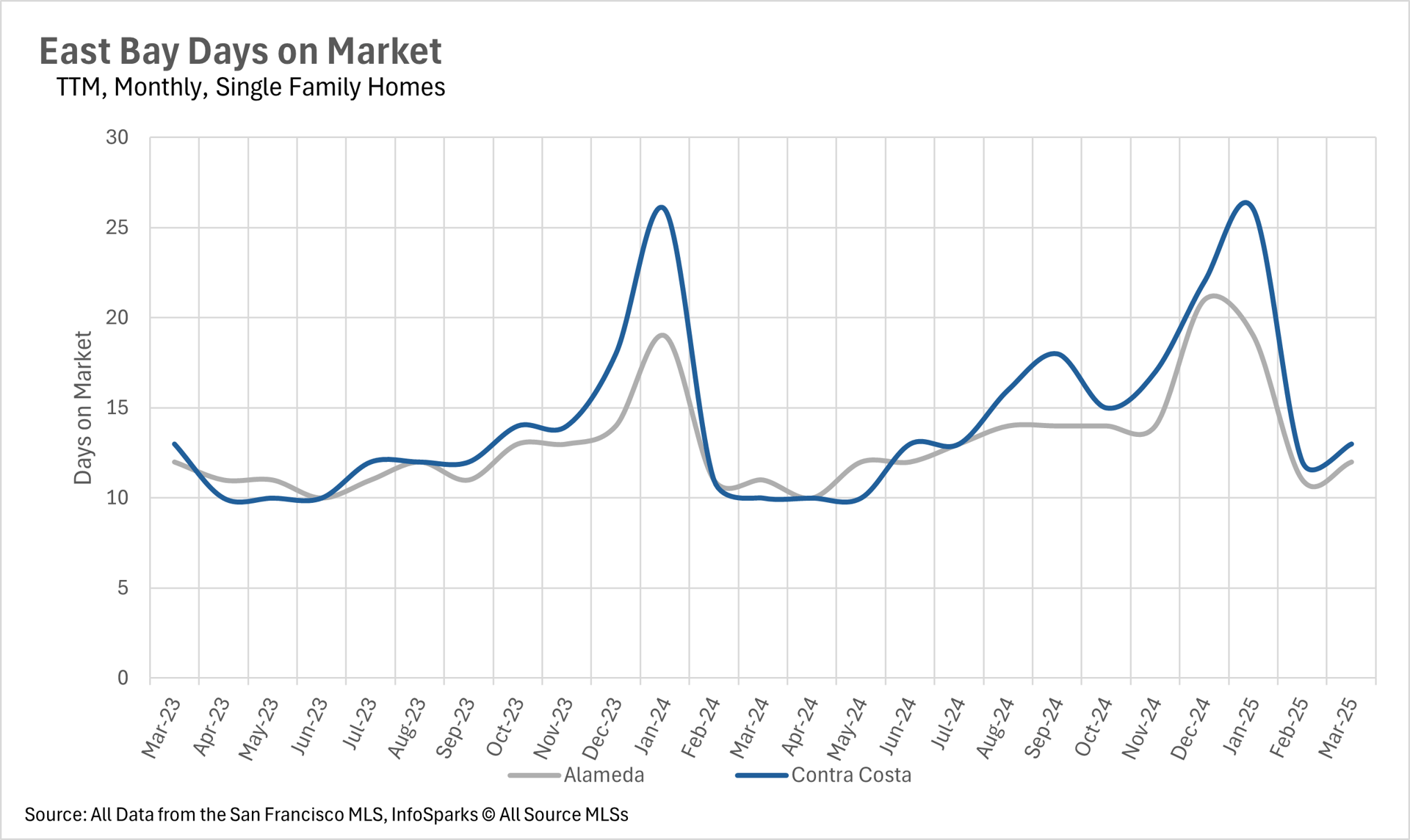

Although inventories have built up quite a bit over the past couple of months, homes are still moving relatively quickly, with the average listing in Alameda and Contra Costa Counties only lasting 12 and 13 days, respectively, before being purchased!

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

Median sale prices have dipped slightly throughout the East Bay

In the month of March, median sale prices dipped by 4.41% and 7.44% in Alameda and Contra Costa counties, respectively. This was largely due to the fact that we’ve seen a huge influx of inventory over the past couple of months. Unfortunately, there simply isn’t enough demand for all of the new supply hitting the market, which is causing prices to decrease. It is important to note though, the overall trend in pricing is in line with what you might typically expect. The decreases in sale price that we’re seeing are on a year-over-year basis, there was still a considerable increase in price on a month-over-month basis!

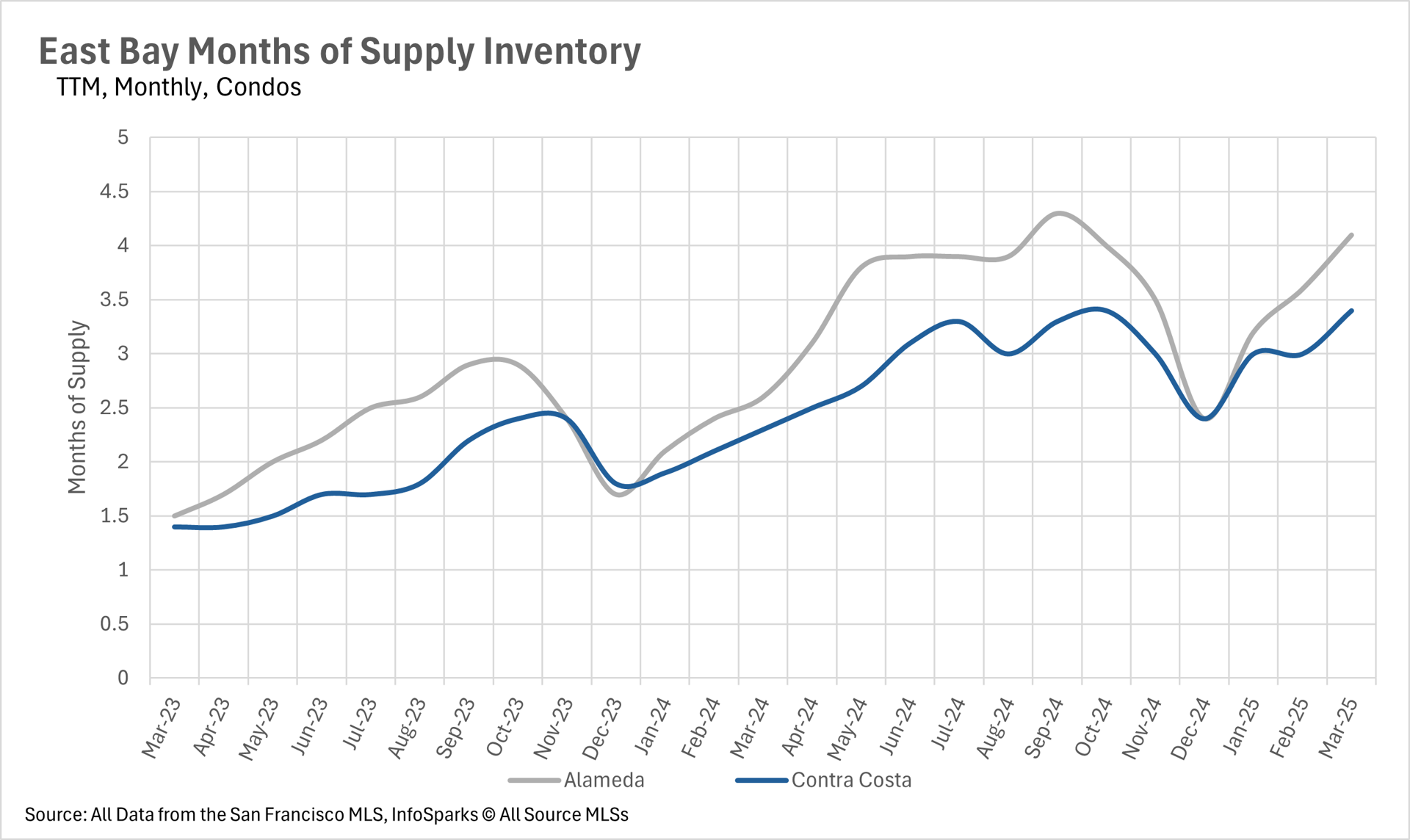

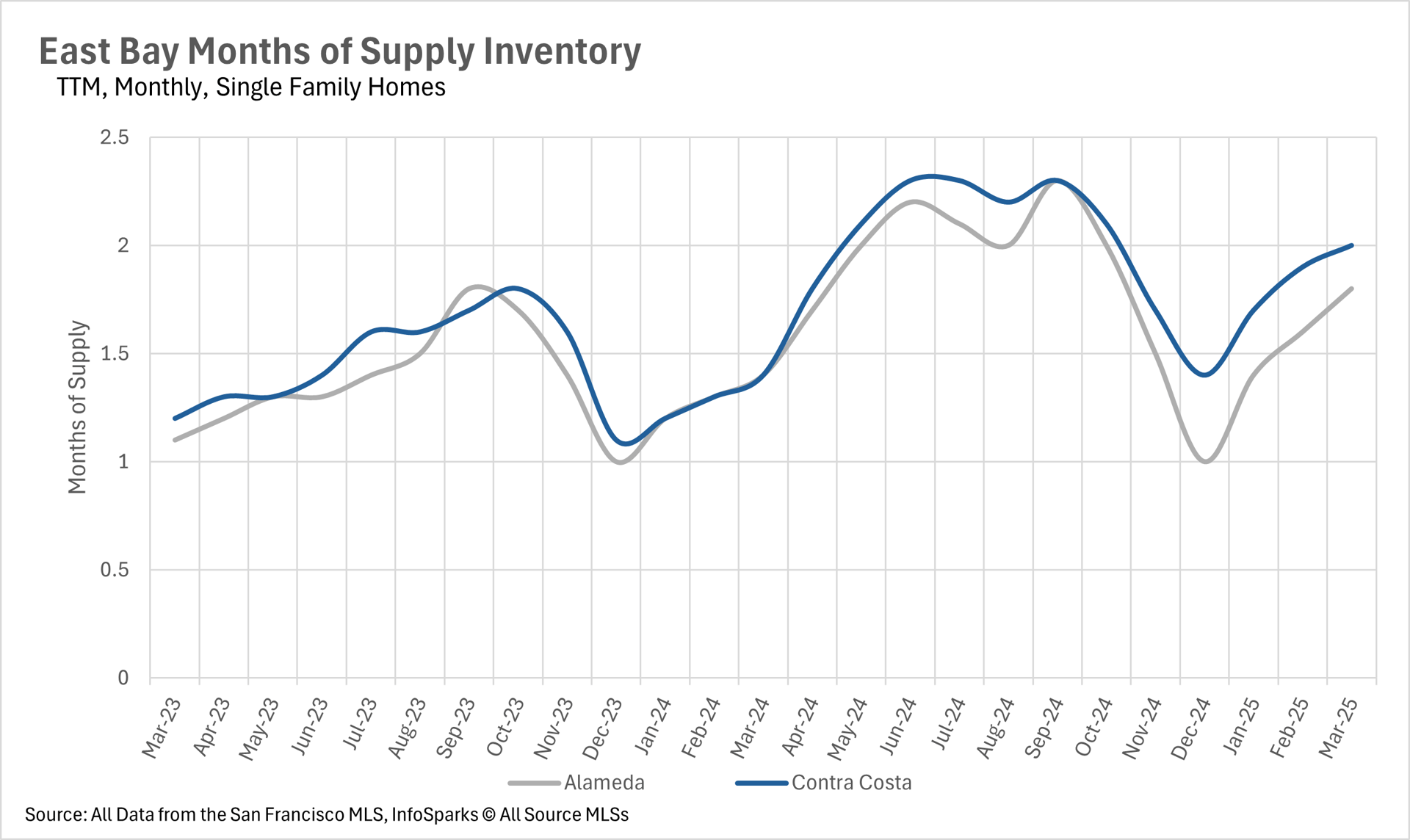

East Bay inventory levels remain incredibly high

Throughout 2025, we’ve seen a ton of inventory added to the market, and that trend certainly continued throughout March, as 2,046 new single-family homes hit the market! This represents a 16.78% increase over last March. However, demand could not keep up with all of the new supply hitting the market. 1,232 homes were sold throughout the month of March, which only represented an 11.59% increase compared to last year.

When you combine the fact that more supply was added in the month of March than sold with the fact that there has been an unprecedented number of homes listed so far this year, you have a recipe for a drastic increase in inventory. This is exactly what we’re seeing, as the number of active listings is up by 47.79% when compared to March 2024!

Despite high inventory levels, homes are still moving quickly!

When you see that there’s nearly 50% more inventory than there was last year, and nowhere near a 50% increase in demand, you might think that homes are sitting on the market for extended periods of time. However, that couldn’t be further from the truth in the East Bay. The average home is only sitting on the market for 12 days in Alameda County and 13 days in Contra Costa County. Although these figures are certainly up from last year, that’s still an incredibly short amount of time for a home to sit on the market!