January 2022 East Bay Market Update

Real Estate

Real Estate

Our team is committed to continuing to serve all your real estate needs while incorporating safety protocol to protect all of our loved ones.

In addition, as your local real estate experts, we feel it’s our duty to give you, our valued client, all the information you need to better understand our local real estate market. Whether you’re buying or selling, we want to make sure you have the best, most pertinent information, so we’ve put together this monthly analysis breaking down specifics about the market.

As we all navigate this together, please don’t hesitate to reach out to us with any questions or concerns. We’re here to support you.

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

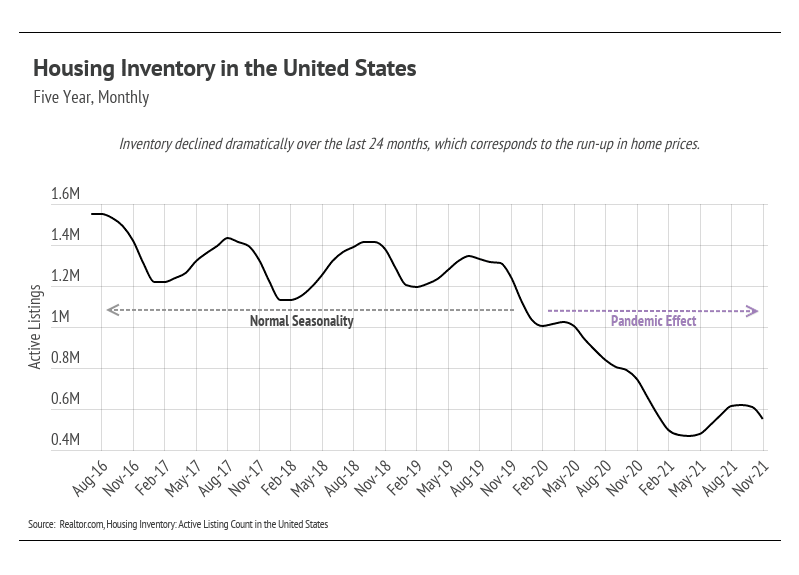

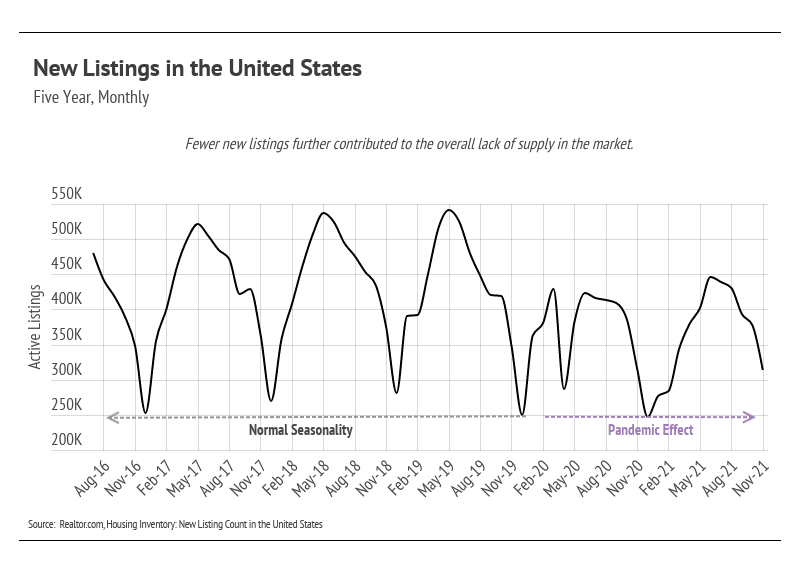

The driving force behind the substantial price increases over the past two years has been the supply of homes, or lack thereof. So, will the housing shortage reverse? The answer is no, as there is no reasonable scenario that would bring active listings to pre-pandemic norms. Before February 2020, seasonal inventory typically peaked in the summer months, but it was trending slightly lower each year. In 2016, inventory peaked at 1.55 million active listings, and by 2019, the peak fell to 1.35 million homes. Inventory in 2021 reached its highest point at approximately 621,000, a 54% decline over two years. Homebuilders simply cannot build fast enough, especially in sought-after urban areas that have already been developed, and new listings are peaking far lower than the historical seasonal norms.

At the same time, we are on pace to see around a million more homes sold in 2021 than in a typical year, based on the long-term average. In other words, more homes are selling, despite the historically low inventory, which is further driving down inventory. In 2022, we expect demand to remain elevated and supply depressed, which should keep home prices from depreciating.

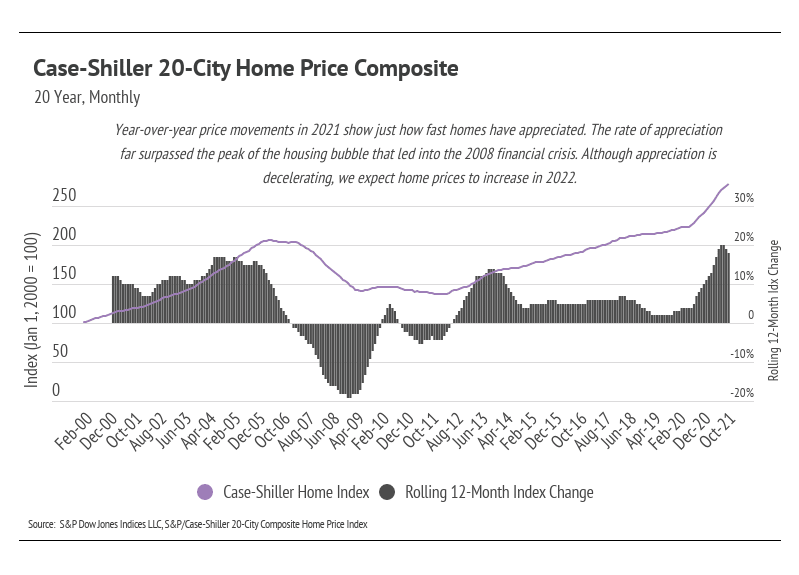

Price appreciation likely will not see the record gains we experienced over the past two years, which is actually good. If we learned one thing from the mid-2000s, we know that we don’t want another housing bubble. The deceleration in price increases, therefore, actually benefits the current market. From a practical standpoint, home prices rising at 20% per year is unsustainable and would certainly cause a major collapse. Moving through 2022, we expect year-over-year price increases to move back to historical norms, in the 5–10% range.

Fed rate hikes in 2022 could drastically affect appreciation as well, which, again, isn’t a bad thing. The low-cost financing we’ve seen over the past two years could be coming to an end (although it’s difficult not to take a believe-it-when-I-see-it-approach to rate increases). When we account for current inflation, which is the highest it’s been since 1981, the real rate of borrowing is negative if you borrow at a rate below 6.8%. Simply put, you’re getting paid to borrow! We don’t expect this phenomenon to last long — it’s a fairly unique situation.

The market remains competitive for buyers, but conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly.

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

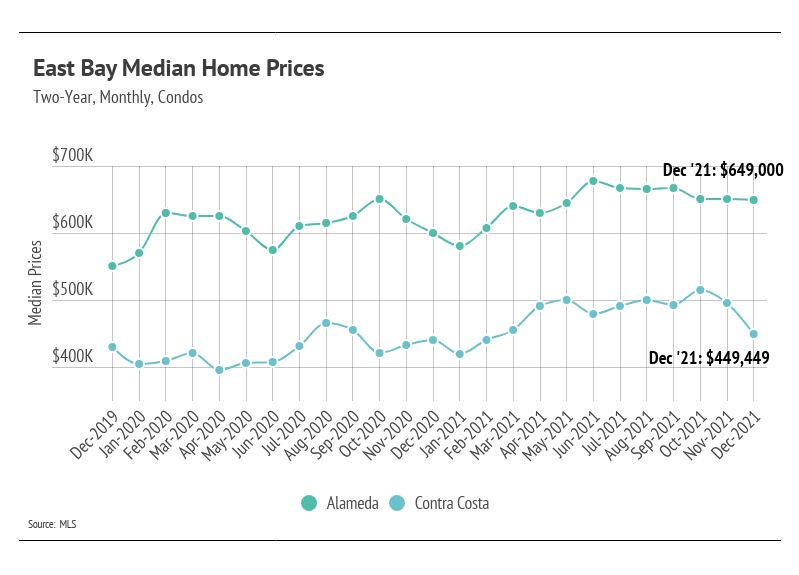

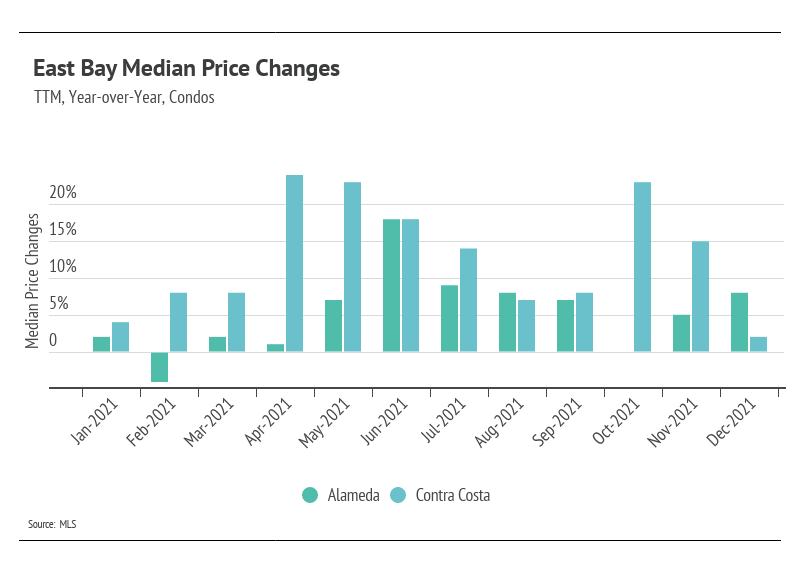

After single-family home prices appreciated significantly in the first half of 2021, it makes sense that prices declined in the third and fourth quarters. Although Alameda home prices have been historically high, they’ve declined over the past four months. Contra Costa home prices experienced a much larger price correction after the May peak, declining 17% from May to December. Condo prices finished the year with smaller price gains.

The East Bay market does seem to be cooling, which is a seasonal norm this time of year. However, with inventory at record lows, we could easily see prices start to rise once again in 2022, especially in the spring and summer seasons.

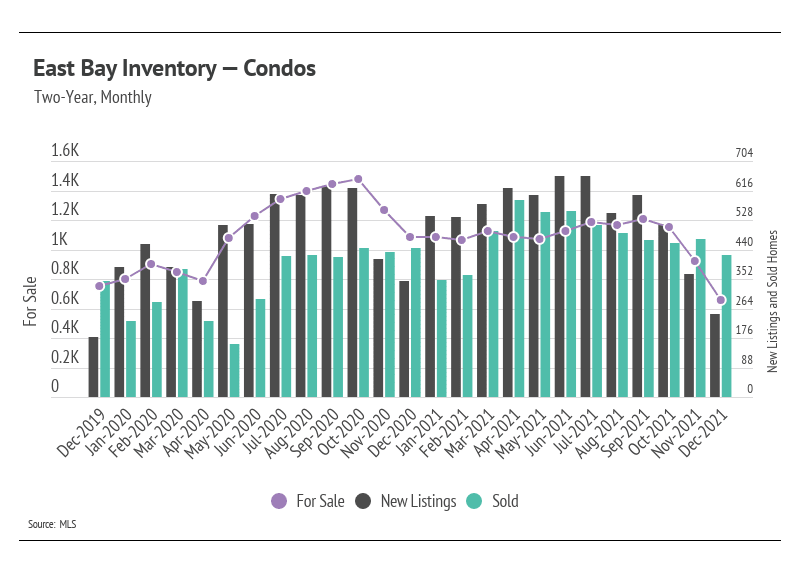

Despite the slight increase in single-family home and condo inventory in the first half of 2021, the sustained high demand and lack of new listings in the second half brought single-family home and condo supply to historic lows. Once again, we are seeing that far more people want to live in the East Bay than want to leave. Sales in the East Bay have been incredibly high, especially when accounting for available inventory, again highlighting demand in the area. Sellers can expect multiple offers, and buyers should come with competitive offers.

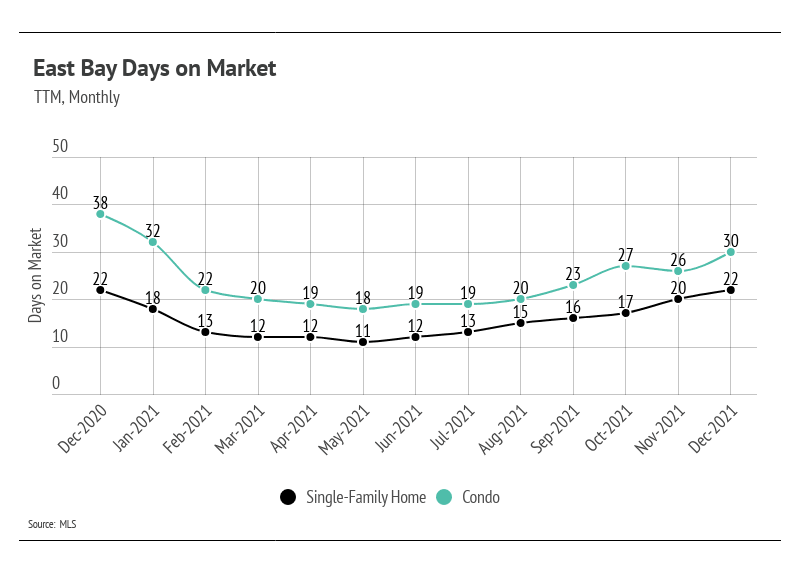

Homes are still selling extremely quickly. Days on Market is rising slightly, but this is more a function of seasonality than a lack of demand for homes. Buyers must put in competitive offers, which, on average, are about 6–12% above list price.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes for sale on the market to sell at the current rate of sales. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). Currently, single-family home and condo MSIs are both historically low, indicating a sellers’ market.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.